Fund Management Charges in ULIP:- These charges are levied for managing your funds. This is charged by the insurer as a percentage of the fund’s value and is deduced before computing the net asset value of the fund. According to IRDAI regulations, it should not be more than 1.5%.

How many types of charges are there in ULIP plan?

Insurance companies have often found themselves at the receiving end for imposing stiff fees or costs since these charges shrink the investible portion of the premium paid. This battle raged prominently in the case of unit linked insurance plans, or ULIPs, for years.

Which bank is best for ULIP?

INSURER FUND CATEGORY Filter

| ULIP Scheme | Category | 2Y |

|---|---|---|

| PNB MetLife – Met Wealth Plus – Virtue II | Large-cap oriented funds | 37.50% |

| PNB MetLife – Met Smart One – Virtue II | Debt long term funds | 37.50% |

| AEGON Life iMaximize Plan – Opportunity Fund | Large-cap oriented funds | 33.00% |

Can I withdraw ulip after 5 years?

ULIP is a long-term investment game. You can exit from ULIP after 5 years; however, it is not advisable even after lock-in period ends. To reap the benefits, you should continue and stay invested for a long period say 15-20 years.

How is ULIP calculated?

Now, there will be a ULIP NAV. The new NAV can be calculated by dividing Rs 100,000 by 8,910 (as the number of units in the fund remains unchanged). This means the new value of each unit in the fund is now Rs 11.22, and both Aditya and Astha will make a profit of Rs 1.22 per unit.

What is mortality charge in ULIP?

What is mortality charge in ULIP? When an individual subscribes to a ULIP , the insurer levies a charge for insurance protection upon his death and to cover other expenses, known as mortality charge. It is usually deducted along with other charges, before investing the policyholder’s money.

How FMC is calculated?

The FMC is adjusted from NAV on a daily basis. The maximum allowed is 1.35 percent per annum of the fund value and is charged daily. Generally, insurers levy the maximum allowed in equity funds, while the charge on non-equity funds are lower.

What is the lock in period for ULIP?

5 years

ELSS vs ULIP – Comparative Analysis

| Particulars | ULIP (Unit Linked Insurance Plan) |

|---|---|

| Lock-in period | ULIPs have a mandatory lock-in of 5 years |

| Returns | The returns can vary because an investor can choose any combination of equity, debt, hybrid funds in his investment. |

Is ULIP income taxable?

You can claim income tax deductions on the amount invested u/s 80C of the Income Tax Act in the case of ULIP. But the gains are taxable. Whereas, long-term capital gains arising from ELSS is taxed at 10% beyond Rs. 10 lakh.

Why is ULIP not good?

The problem with the ULIP is you neither get decent returns nor do you get decent insurance coverage. An investor has the option of choosing where your premium is invested in an ULIP. Your premium can be invested in equity mutual funds, debt mutual funds or a combination of both.

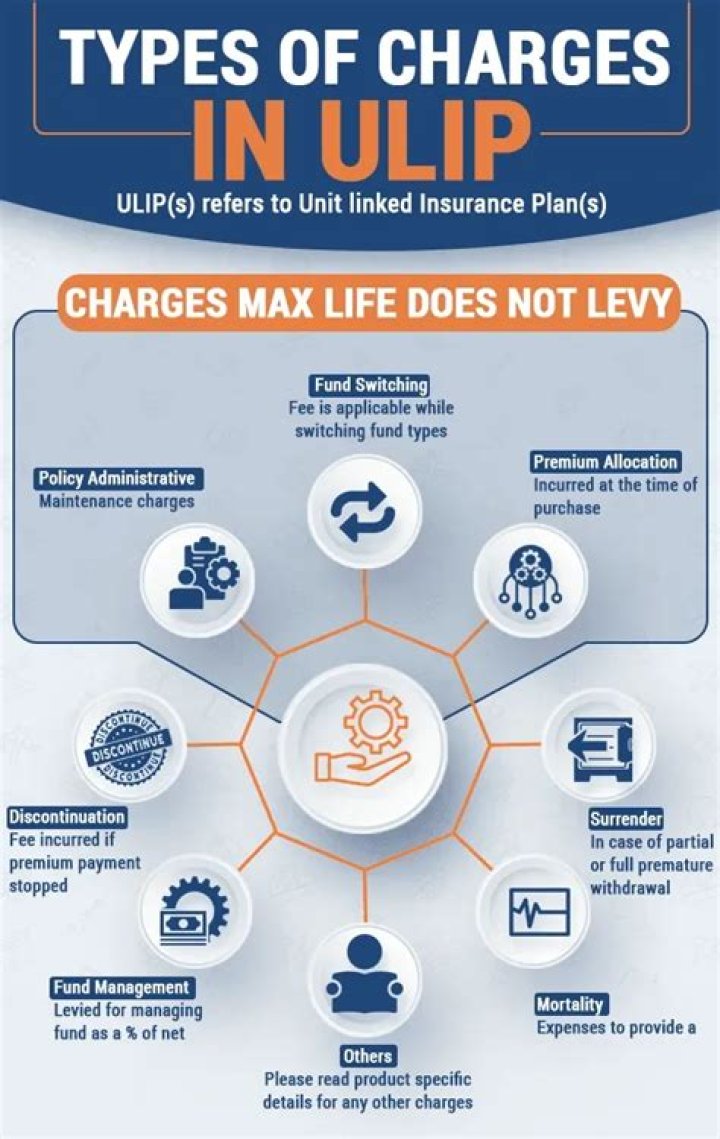

What are the major charges in ULIP?

Here are the major ULIP charges:- Premium Allocation Charges in ULIP :- It is a percentage of the first year premium charged by the insurer before allocating the policy. These are the initial expenses incurred by the insurance company at the time of policy issuance.

What is the premium break-up under a ULIP policy?

It is important that you understand the premium break-up under your Unit Linked Insurance Policy. Once you decide the amount of premium to be paid and the Life Cover you want, the insurance company deducts a portion of the ULIP premium. This portion is called the Premium Allocation Charge, and varies from product to product.

How is the ULIP withdrawal amount calculated?

It is calculated by the insurer after factoring in your age, health risk and mortality table used by the insurer. Switching Charges in ULIP :- An investor is allowed a fixed number of free switches between different fund options every year.

What is ULIP and how to invest in it?

As ULIP is an insurance cum investment product, it is important for insurance holders to review the performance of the funds over the long-term. In a ULIP plan, the policyholder can invest in equity, balanced or debt fund as per their risk appetite and investment time horizon.